Life insurance is typically viewed as protection — something that pays a benefit in the future. What many policyowners don’t realize is that under the right circumstances, a life insurance policy can also function as a valuable financial asset today.

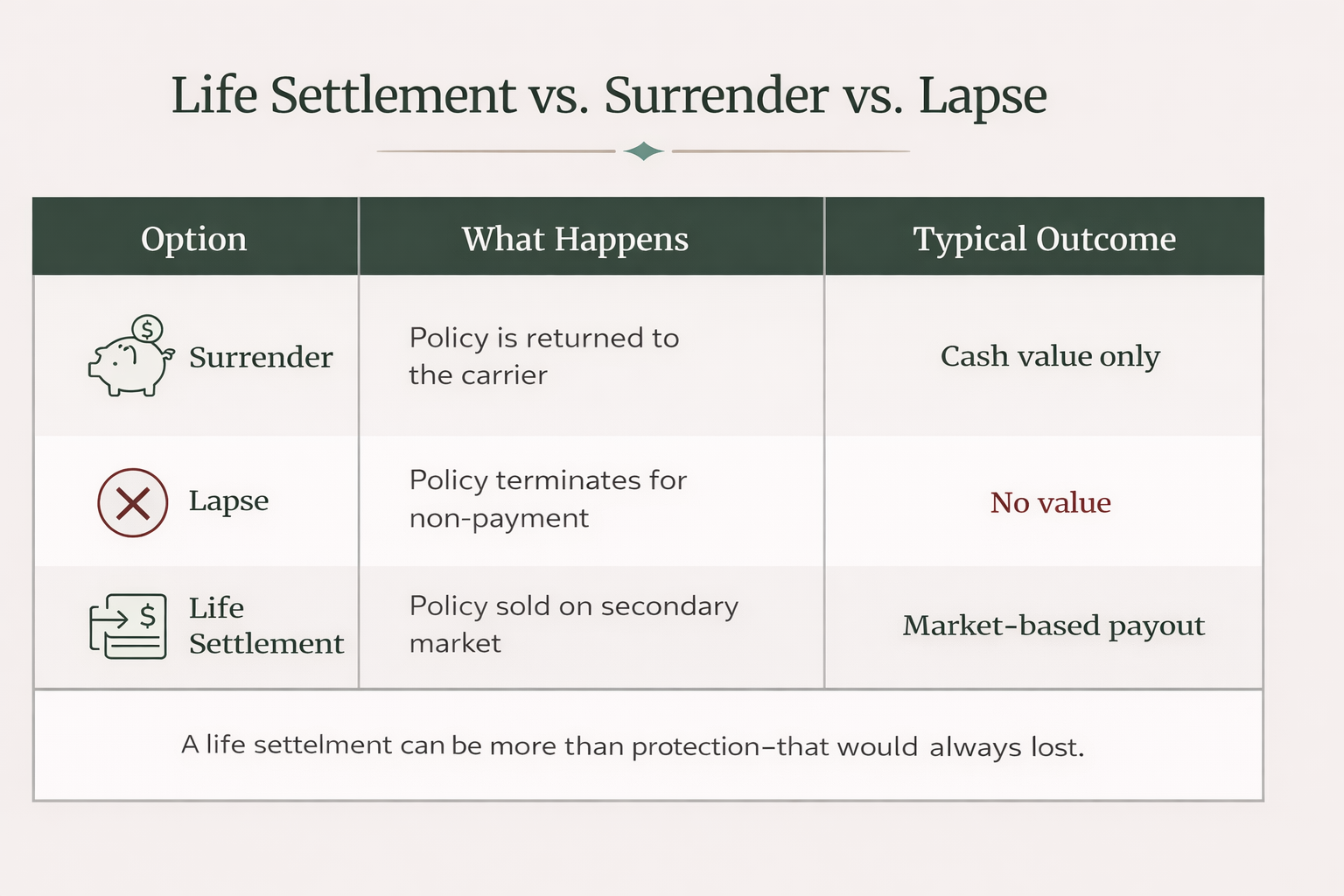

A life settlement allows qualifying policyowners to sell an existing life insurance policy to a third party for more than its cash surrender value, providing immediate liquidity when coverage is no longer needed or premiums have become burdensome.

At Living Equity Group, we help clients and advisors evaluate whether a life settlement is appropriate by objectively reviewing policies, market options, and long-term planning considerations.

A life settlement is the sale of an in-force life insurance policy to a licensed third-party investor. In exchange, the policyowner receives a lump-sum payment that is typically greater than the policy’s cash surrender value, but less than the death benefit.

After the transaction:

Life settlements are regulated transactions governed by state insurance laws, with consumer protections and disclosure requirements in place.

While each case is unique, most life settlement evaluations follow a structured process:

The policy’s type, face amount, premium structure, carrier, and in-force performance are reviewed.

Medical records are evaluated to estimate life expectancy, a key factor in settlement valuation.

Qualified settlement providers assess the policy and submit bids based on risk, premium requirements, and expected duration.

Offers are compared against alternatives such as surrender, lapse, or restructuring the policy.

Once accepted, ownership transfers and the policyowner receives proceeds.

Throughout this process, proper disclosure and advisor coordination are essential.

Life settlements are not appropriate for every policyowner. However, they are commonly considered in situations such as:

In many cases, policyowners would otherwise surrender or lapse a policy — often leaving significant value unclaimed.

While eligibility varies, life settlements are most often associated with:

Each case is evaluated individually.

Tax treatment of life settlement proceeds depends on factors such as:

Proceeds may be taxed as a combination of:

Because tax treatment can vary, coordination with a CPA or tax advisor is strongly recommended. Living Equity Group does not provide tax advice.

Before pursuing a life settlement, policyowners should consider:

A settlement should be evaluated in the context of the full financial picture — not in isolation.

At Living Equity Group, we approach life settlements as part of a broader planning conversation — not a one-off transaction.

We provide:

Our role is to help determine whether a life settlement makes sense — not to push a predetermined outcome.

Life settlements often intersect with:

Exploring all available options ensures decisions are informed and intentional.

A life insurance policy can be more than protection — in the right circumstances, it can be a financial asset with real market value. Before surrendering or lapsing a policy, it’s worth understanding all available options.

Not sure if your policy qualifies for a life settlement?

We can review your policy and help determine whether a life settlement aligns with your goals.

→ Request a Policy Review