Indexed universal life provides permanent coverage and a way to credit interest linked to external market indexes. The policy does not invest directly in the index. Credited interest is subject to a floor that helps limit negative credits and to carrier terms such as caps, participation rates, or spreads.

Get StartedPremiums support insurance costs and policy expenses. The remainder goes towards building the policy’s cash value. You can allocate cash value among a fixed account and one or more index accounts. At the end of each crediting period the carrier applies the contract terms to determine the interest credit.

Minimum credited rate for the period. Many designs use a 0% floor.

A cap limits the upside for the period. A participation rate credits a percentage of the index change. Some designs use both.

A stated amount or percentage that is subtracted before interest is credited.

.png)

IUL provides access to cash value through withdrawals and policy loans. Withdrawals and loans reduce policy values and death benefit and can cause a policy to lapse if not managed carefully.

Remove a portion of cash value. May reduce the face amount depending on policy provisions.

Fixed or variable loan rate. Loaned values usually come out of index accounts to a loan account.

Loaned values can continue to receive indexed credits based on carrier rules. The net cost depends on loan rate and crediting performance.

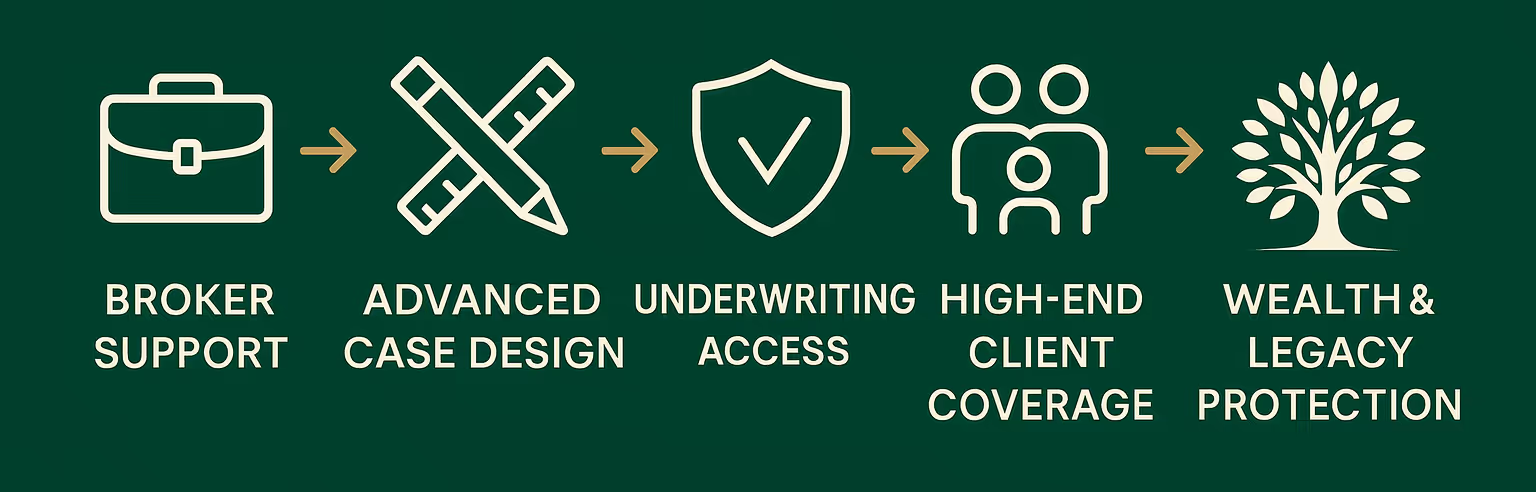

Our advanced case design team models multiple carriers and strategies. We include current rates and illustrate conservative ranges. We run historical lookbacks for common allocations and test alternate premium patterns, policy loans, and rider selections. You receive a clear side-by-side analysis that shows how choices affect long-term outcomes.

From initial consultation through policy management, we provide clarity, transparency, and ongoing support — giving you a policy that performs in both the short and long term.

Work with our advanced case design team.Request an objective comparison that shows caps, floors, costs, and distribution strategies across leading carriers.

Request IUL Illustrations