For business owners, life insurance is far more than a death benefit. It's a strategic financial tool that solves succession challenges, protects key employees, funds buy-sell agreements, and creates tax-advantaged access to policy values in retirement when designed correctly. When structured properly, permanent life insurance becomes a cornerstone of business continuity and personal wealth preservation.

This guide examines how business owners leverage life insurance across five critical areas: succession planning, key person protection, executive compensation, estate tax mitigation, and personal retirement income. Each strategy includes implementation frameworks, carrier considerations, and case examples with specific numbers where applicable.

Who this article is for: Business owners with partners or co-shareholders, high-income earners who've maxed out qualified retirement plans, and owners of businesses valued above $2 million facing succession or estate tax planning challenges. If you're a solo entrepreneur with under $500k in annual revenue and no partners, simpler term life insurance strategies may be more appropriate.

Traditional life insurance solves one problem: replacing income when someone dies. But business owners face a different set of risks. What happens to the business if a partner dies unexpectedly? How do you retain top executives without equity dilution? How do you extract wealth from the business without triggering massive tax liabilities?

These questions don't have simple term life insurance answers. They require sophisticated permanent life insurance structures that integrate with business operations, partnership agreements, and long-term wealth planning.

The five core use cases for business owners:

Each strategy uses different policy types, funding structures, and ownership arrangements. Understanding which tool fits which problem is essential to avoiding costly mistakes.

Use this framework to identify which strategies apply to your specific circumstances:

If you have business partners or co-shareholders → Buy-sell agreement funding with GUL (cross-purchase or entity purchase structure)

If one person drives significant revenue or has irreplaceable expertise → Key person insurance with term or permanent coverage

If you need to retain executives without diluting ownership → Executive bonus plan (Section 162) using IUL or whole life

If your estate exceeds $15 million and the business is your primary asset → ILIT-owned GUL for estate tax liquidity

If you've maxed 401(k) contributions but need more tax-advantaged retirement savings → Overfunded IUL with policy loan strategy (understand the risks first)

If you face multiple challenges → Integrated strategy combining buy-sell, key person, and personal retirement planning

The sections below explain each strategy in detail, including structure, tax treatment, carrier selection, and implementation considerations.

When a business partner dies, retires, or becomes disabled, the surviving owners need capital to buy out their interest. Without a funded buy-sell agreement, this forces either outside investors (diluting control) or business liquidation (destroying value).

Life insurance solves this by creating instant liquidity at the exact moment it's needed.

Cross-purchase agreements have each owner buy policies on the other partners. When one dies, the surviving owners personally receive the death benefit and use it to buy the deceased partner's shares.

Entity purchase agreements have the business itself own policies on all partners. When a partner dies, the company receives the death benefit and redeems the deceased owner's shares.

Tax treatment differs significantly:

In a cross-purchase structure, the surviving owners get a stepped-up cost basis on the purchased shares equal to the purchase price. This means lower capital gains taxes if they later sell the business.

In an entity purchase structure, there is no step-up in basis for the surviving owners. The business redeems the shares, but the remaining owners' cost basis stays the same. However, entity purchase is administratively simpler because the company owns all policies.

For buy-sell funding, most business owners use guaranteed universal life (GUL) rather than whole life or indexed universal life. Here's why:

GUL provides:

Typical carriers used: AIG, Banner, Pacific Life, Lincoln Financial, John Hancock

When to use term life instead: If the buyout is only needed for 10-20 years (such as when a succession plan to the next generation is already in place), convertible term life with a conversion rider can work. This gives flexibility to convert to permanent coverage later if circumstances change.

The policy death benefit should match the business valuation formula in the buy-sell agreement. Common approaches include:

Real example: Three equal partners in a professional services firm valued at $6 million. Each partner needs $2 million in coverage. In a cross-purchase structure, each partner owns two policies ($2M on partner A, $2M on partner B). Total of six policies across three people.

Premium cost (illustrative only): For a 45-year-old standard non-tobacco male, a $2 million GUL policy to age 121 might cost approximately $2,500-$3,500 annually depending on carrier and specific product design. This is an illustrative range only and varies materially by underwriting class, health profile, and current interest rate environment. Use a current illustration with actual underwriting for accurate pricing.

The premiums are a business expense that ensures clean ownership transition without forcing liquidation or outside financing.

Death isn't the only trigger event that requires a buyout. What happens if a partner becomes totally and permanently disabled and can no longer contribute to the business?

Disability buyout insurance funds the purchase of a disabled partner's ownership interest, typically after a waiting period (12-24 months of disability). This prevents a situation where the disabled partner remains on the cap table but can't contribute, creating friction with active partners who are running the business.

Structure: Disability buyout policies are separate from buy-sell life insurance and require underwriting for disability coverage. They're typically structured as individual policies owned by each partner (similar to cross-purchase for life insurance) or as a business overhead expense policy that funds the buyout.

Cost consideration: Disability buyout coverage is significantly more expensive than life insurance because the probability of disability before retirement is much higher than the probability of death. Expect premiums to be 3-5 times higher than comparable life insurance coverage.

This is a common gap in business succession planning. Address it when structuring your buy-sell agreement.

Losing a top executive, rainmaker salesperson, or technical expert can devastate a business. Key person insurance provides capital to:

The rule of thumb is to insure key employees for 5-10 times their annual compensation, but this varies widely based on their actual contribution to revenue.

Better approach: Calculate the economic impact of losing this person:

Example: A rainmaker partner generates $5 million in annual revenue with a 30% profit margin. That's $1.5 million in annual profit. If replacement takes two years, the economic loss is $3 million, plus $500k in recruitment costs. Total key person coverage needed: $3.5 million.

The business owns the policy, pays the premiums, and receives the death benefit. Premiums are not tax-deductible as a business expense. The death benefit is generally received income tax-free by the company, subject to IRC Section 101(j) compliance.

Critical compliance issue: For employer-owned life insurance policies (including key person coverage), the death benefit income tax exclusion can be limited or eliminated if you don't comply with IRC Section 101(j).

Requirements include:

Exceptions and eligibility: Exceptions and eligibility categories exist under IRC 101(j), but don't rely on a blog summary. Confirm the insured's status, documentation timing, and reporting requirements with counsel/CPA before policy issue. The safest default is to complete notice-and-consent properly for every employer-owned policy and file Form 8925 annually.

Consequence of non-compliance: If these requirements aren't met, the death benefit is taxable as ordinary income to the extent it exceeds premiums paid.

Action required: IRC 101(j) compliance must be handled with legal counsel and your CPA before purchasing employer-owned life insurance. This is not optional.

For large C corporations: If you're a large C corporation that may fall under the Corporate Alternative Minimum Tax (CAMT) rules, have your CPA model the financial-statement income impact of death benefit proceeds.

Most businesses use term life insurance for key person coverage because:

When to use permanent coverage: If the key person is also a partner or owner, combining key person protection with buy-sell funding justifies permanent coverage. The policy can be converted to personal coverage when the person retires or leaves the business.

Typical carriers used: Most major carriers (Banner, Pacific Life, AIG, LSW, Nationwide, John Hancock) offer competitive term life rates. These carriers are frequently used because they offer high face amount capacity ($10M+), competitive underwriting for business owners, and financial strength ratings of A or better.

Pricing is determined by age, health class, and coverage amount. For business owners, working with an agency that has relationships across multiple carriers ensures you get the best underwriting outcome rather than being limited to a single carrier's risk assessment.

Small and mid-sized businesses often struggle to compete with larger companies for executive talent. Offering equity dilutes existing ownership, but traditional bonuses are heavily taxed and don't create long-term retention.

Executive bonus plans (Section 162 plans) solve this by using permanent life insurance as a deferred compensation vehicle.

Tax treatment:

The premium payment is taxable income to the executive in the year paid. However, the cash value grows tax-deferred, and the executive can access it via tax-free policy loans in retirement. This creates a better long-term outcome than receiving the same amount as cash compensation.

Example: A $50,000 annual bonus paid in cash to an executive in a 40% combined tax bracket nets $30,000. The same $50,000 paid as life insurance premiums creates cash value that can grow to $400,000+ over 20-30 years, depending on policy structure and performance.

Scenario: Software company wants to retain VP of Engineering for 10 years until acquisition exit.

Structure:

What happens if they leave year 3:

Tax treatment on repayment: When the executive repays unvested bonuses to the company, they may be able to claim a deduction for the repayment (consult tax advisor). The company treats the repayment as a reduction of prior compensation expense.

Legal requirement: Repayment agreements must be carefully drafted to be enforceable under state employment law. Some states limit the ability to require repayment of compensation. This must be reviewed by employment counsel before implementation.

Indexed Universal Life (IUL) is most commonly used for executive bonus plans because:

Whole life works better for conservative executives who want guaranteed growth and dividends rather than market-linked performance.

Carriers frequently used: Nationwide, Pacific Life, John Hancock, AIG, Lincoln Financial (LSW)

To prevent an executive from taking the policy and leaving immediately, companies often structure these plans with:

These provisions should be reviewed by legal counsel to ensure they're enforceable in the company's state.

Business owners with estates above the federal estate tax exemption ($13.99 million per person in 2025, increasing to $15 million in 2026 per legislation signed July 4, 2025, with inflation indexing thereafter) face a critical problem: estate taxes are due within nine months of death, but the estate's main asset (the business) is illiquid.

Note: Estate tax laws can change with new legislation. These figures are current as of February 9, 2026, but should be verified with a tax advisor when implementing estate planning strategies.

This forces heirs to either:

Life insurance provides immediate liquidity to pay estate taxes without forcing a business sale.

To keep life insurance proceeds out of the taxable estate, the policy must be owned by an Irrevocable Life Insurance Trust (ILIT) rather than by the business owner personally.

How ILITs work:

Annual gift tax exclusion: In 2025, an individual can gift $19,000 per beneficiary without using lifetime exemption. A married couple with three children can gift $114,000 annually to an ILIT without gift tax consequences.

Guaranteed Universal Life (GUL) is the most cost-effective solution for estate tax planning because:

Example: A 55-year-old business owner with a $20 million estate and estimated $4 million estate tax liability. A $4 million GUL policy might cost $35,000-$50,000 annually depending on health class and carrier.

Second-to-die policies (survivorship life) are often used for married couples because estate taxes aren't due until the second spouse dies. Second-to-die policies cost significantly less than insuring one life because the death benefit isn't paid until both insureds have passed away.

Preferred carriers: Pacific Life, AIG, Banner, LSW, John Hancock, Nationwide (for second-to-die GUL products)

Underwriting consideration: Estate planning cases often involve older, higher-net-worth individuals. Working with carriers that specialize in high face amount policies and have streamlined underwriting for affluent clients makes the process faster.

Business owners often max out 401(k) and profit-sharing contributions but still need additional retirement income. Traditional brokerage accounts create taxable distributions. Roth IRAs have income limits that exclude high earners.

Indexed Universal Life (IUL) can create tax-advantaged retirement income through policy loans when structured properly and maintained correctly.

Tax advantage: Policy loans are not considered taxable income as long as the policy remains in force. This creates a tax-free income stream in retirement that doesn't count toward adjusted gross income, preserving Medicare subsidies and avoiding taxation of Social Security benefits.

Client profile:

Policy structure:

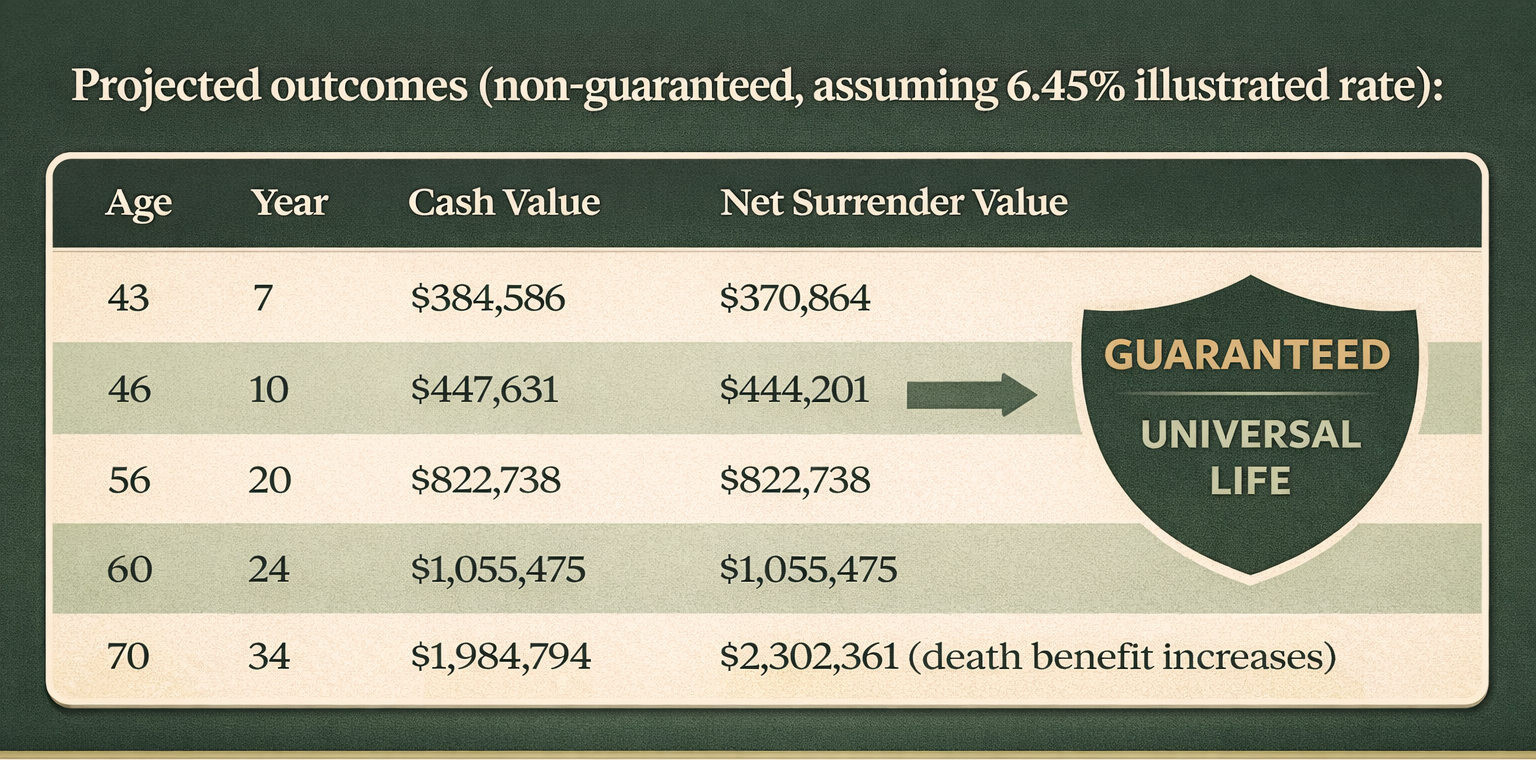

Projected outcomes (non-guaranteed, assuming 6.45% illustrated rate):

Key insights:

After 7 years of funding at illustrated performance levels, additional premiums may not be required. Whether the policy becomes self-sustaining depends on actual credited interest rates matching or exceeding illustrated rates and policy charges remaining at current levels.

Starting at year 11 (age 47), the client can begin taking tax-advantaged policy loans (when structured properly and the policy remains in force). If he takes $40,000 annually from age 60-85, the policy may still maintain over $1 million in death benefit, depending on actual performance and loan activity.

Illustrations are not guarantees. The projections above assume a 6.45% illustrated crediting rate that may never be achieved. Actual performance depends on:

Cap and participation rate changes: Carriers can adjust caps, participation rates, and spreads annually within contractual limits. Current cap rates (10.25% on Nationwide's S&P 500 strategy) can and do change. Verify current rates at policy design time.

Rising cost of insurance charges: COI charges increase with age and can rise within guaranteed maximum limits stated in the policy contract. If actual charges exceed illustrated charges, additional premiums may be required.

Loan arbitrage risk: Policy loans typically charge 3-5% interest while credited rates vary. If loan interest exceeds credited interest for extended periods, the policy can enter a death spiral requiring additional premiums or risk of lapse.

Lapse risk creates taxable income: If the policy lapses with outstanding loans, the loan balance becomes taxable income in the year of lapse. This can create a six-figure tax liability with no cash to pay it.

Market performance risk: Even with 0% floors, consecutive years at or near 0% credited interest while loan interest compounds can rapidly erode cash value.

Required actions to maintain the strategy:

Why this can work better than a Roth IRA (when managed properly):

To maintain tax-advantaged loan treatment, the policy must not become a Modified Endowment Contract (MEC) under IRC Section 7702A.

MEC rules (7-pay test): If cumulative premiums in the first 7 years exceed the IRS-defined premium limit (the "7-pay premium"), the policy becomes a MEC. Distributions from MECs are taxed as ordinary income and subject to a 10% penalty if taken before age 59½.

This fundamentally changes the tax treatment and destroys the retirement income strategy.

For the case study above: The 7-pay premium limit is $94,234.96. The client pays $50,000 annually, staying well under the MEC threshold.

How to check: Every illustration includes the MEC limit. Premium funding should stay at or below this limit to preserve tax-free loan treatment.

Carriers frequently used: Nationwide, Pacific Life, John Hancock, AIG, Lincoln Financial (LSW)

What to compare:

Cap rates, participation rates, and spreads change periodically. Always verify current rates when designing a policy, as illustrated rates from previous years may no longer be available.

Who owns the policy matters for tax purposes and business continuity.

Individual ownership: The business owner personally owns the policy and pays premiums. This works for personal retirement income strategies but doesn't provide business continuity benefits.

Business ownership: The company owns the policy and pays premiums. This works for key person insurance and entity purchase buy-sell agreements. Premiums are not tax-deductible, but the death benefit is received income tax-free by the business.

Trust ownership: An irrevocable trust owns the policy. This removes the death benefit from the taxable estate for estate tax planning purposes.

Split ownership: In some cases, the business initially owns the policy, then transfers it to the individual at retirement or separation. This allows business expense funding during active years, then personal ownership later.

Critical tax trap: If a life insurance policy is sold or transferred for value, the death benefit becomes taxable income (minus premiums paid).

Exceptions to the transfer-for-value rule:

When transferring policies from business to personal ownership, structure the transfer carefully to avoid triggering this rule. Work with a tax advisor to ensure compliance.

Business owners often have unique underwriting challenges:

High-stress occupations: Some business types (construction, aviation, hazardous materials) trigger higher risk classifications or flat extra charges.

Financial underwriting: For high face amount policies ($5 million+), carriers require financial justification through tax returns, financial statements, or business valuations.

Foreign travel: Business owners with international operations may face travel-related underwriting restrictions, particularly to certain countries.

Net worth requirements: For policies above $10 million, carriers often require minimum net worth (typically 10-20 times the death benefit).

Business owners don't have time for prolonged medical exams and paperwork. Options to streamline underwriting include:

Accelerated underwriting programs: Some carriers (Banner, Pacific Life, John Hancock) offer no-exam underwriting for policies up to $2-5 million if the applicant meets age and health criteria.

Tele-underwriting: Phone interviews replace in-person exams for certain risk classifications.

Concierge underwriting: Some carriers assign dedicated underwriters for high-net-worth cases to expedite processing.

Best practice: Work with an agency like Living Equity Group that has carrier relationships to navigate underwriting efficiently and position the case for the best possible outcome.

1. Underfunding buy-sell agreements: Using outdated business valuations that don't reflect current market value, forcing supplemental financing when a buyout is needed.

2. Mixing personal and business policies: Using the same policy for both estate planning and business succession creates ownership conflicts and potential tax issues.

3. Ignoring policy reviews: Business valuations change. What was adequate coverage five years ago may be 40% too low today. Annual policy reviews should coincide with business valuations.

4. Not coordinating with other advisors: Life insurance strategies should integrate with the business's CPA, attorney, and financial advisor. Disconnected planning creates gaps and inefficiencies.

5. Focusing only on premium cost: The cheapest policy isn't always the best. Carrier financial strength, policy features, and long-term guarantees matter more than saving a few hundred dollars annually.

The right life insurance strategy depends on your specific business structure, partnership agreements, tax situation, and long-term goals.

Questions to ask yourself:

If you answered yes to any of these, a strategic life insurance structure should be part of your business and personal financial plan.

Ready to evaluate which strategy fits your situation?

Living Equity Group specializes in advanced life insurance strategies for business owners. We work with top carriers including AIG, Banner, John Hancock, Lincoln Financial, Nationwide, and Pacific Life to design solutions that integrate seamlessly with your business operations and personal wealth planning.

To properly evaluate your situation and design the right strategy, we'll review:

This information allows us to identify coverage gaps, compare your existing policies to current market options, and design an integrated strategy that addresses succession, protection, and personal wealth planning simultaneously.

Schedule a consultation to review your current coverage and identify gaps →

About Living Equity Group

Living Equity Group provides high-net-worth individuals and business owners with strategic life insurance planning. We don't sell products. We design integrated solutions that solve succession, protection, and tax planning challenges using permanent life insurance as a foundational tool.

Our team handles all backend administration, carrier communication, underwriting coordination, and policy servicing so you can focus on running your business while we ensure your protection and succession plan works exactly as intended.

Questions about implementing these strategies? Contact our team at cases@livingequitygroupllc.com.