When a business partner dies unexpectedly, surviving owners face an immediate problem: they need capital to buy out the deceased partner's interest, but the business's cash is tied up in operations, receivables, and inventory. Without a funded buy-sell agreement, the business either takes on debt, brings in outside investors (diluting control), or faces a forced sale.

Life insurance solves this by creating instant liquidity at the exact moment it's needed. But the structure matters enormously. Cross-purchase, entity purchase, and hybrid approaches have radically different tax consequences, administrative complexity, and long-term implications for the surviving owners.

This guide explains how to structure buy-sell agreements funded with life insurance, calculate the correct coverage amount, choose between cross-purchase and entity purchase models, and avoid common implementation mistakes that create tax liabilities or render the agreement unenforceable.

Who this article is for: Business owners with one or more partners, co-shareholders in S corporations or C corporations, multi-member LLCs taxed as partnerships, and professional practices with multiple equity owners. This applies specifically to closely held businesses where ownership transitions need to be controlled and funded. If you're a solo entrepreneur with no partners, this strategy doesn't apply to you.

A buy-sell agreement is a legally binding contract that dictates what happens to an owner's business interest when a triggering event occurs: death, disability, retirement, divorce, bankruptcy, or voluntary departure.

Not all triggering events should be funded the same way:

Death → Life insurance provides immediate liquidity exactly when needed

Disability → Disability buyout insurance pays after a waiting period (typically 12-24 months) to distinguish temporary from permanent disability

Retirement/voluntary exit → Typically funded through sinking funds, installment payment structures, or bank credit lines rather than insurance

Divorce/bankruptcy → Legal restrictions on forced transfers; agreement should include right of first refusal and valuation provisions but often can't be pre-funded

This article focuses on life insurance funding for death-triggered buyouts, which is the most common and most critical funding need. Disability buyout is addressed separately as a related but distinct risk.

The problem buy-sell agreements solve:

Without a buy-sell agreement, when a partner dies, their ownership interest passes to their estate (typically their spouse or children). The surviving business partners are now in business with the deceased partner's family, who likely have no interest in running the company and want cash instead.

This creates several nightmare scenarios:

Life insurance funding eliminates these problems by ensuring the exact amount needed for the buyout is available immediately upon death, with no debt required.

Buy-sell agreements typically cover multiple triggering events, but they don't all use the same funding source:

Death: Funded with life insurance (the focus of this article). Instant liquidity, no debt required, predictable cost.

Disability: Funded with disability buyout insurance (separate product from disability income insurance). Typically includes a 12-24 month waiting period to distinguish temporary from permanent disability. More expensive than life insurance because disability is statistically more likely than death before retirement.

Retirement / voluntary departure: Usually funded through installment notes paid over 3-7 years, sinking funds set aside annually, or bank lines of credit. Life insurance doesn't apply because there's no insurable event, and the departing partner doesn't need immediate full payment.

Divorce / bankruptcy: Typically handled through forced transfer provisions allowing remaining partners to purchase at formula price, but funded through the same mechanisms as retirement (installment notes or lines of credit). Some states restrict enforceability of buyout provisions triggered by divorce or bankruptcy.

Key insight: A properly funded buy-sell agreement uses multiple funding mechanisms depending on the trigger. Life insurance solves the death problem (which is sudden and creates immediate liquidity needs), but the agreement needs additional provisions for other scenarios.

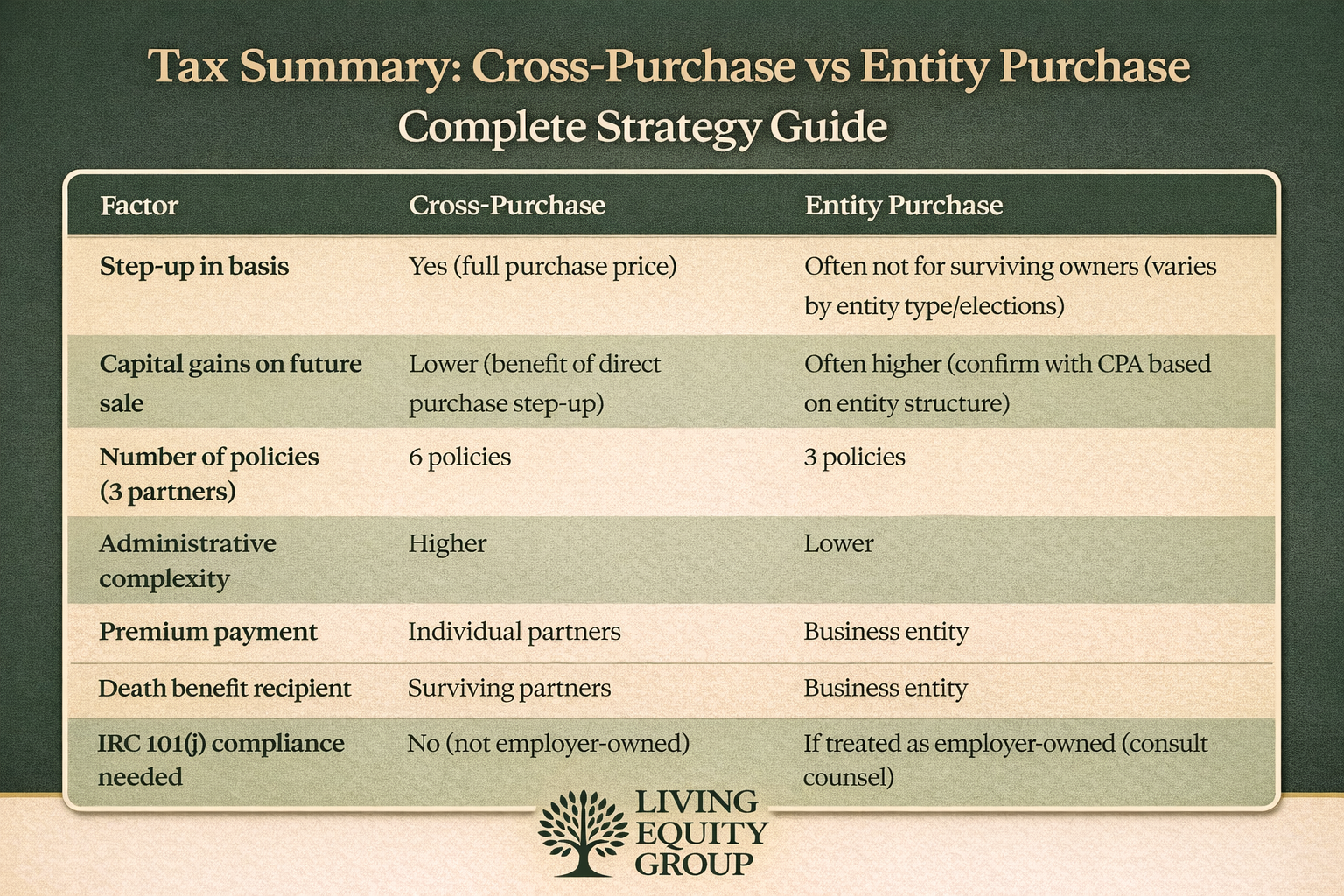

There are two primary structures for life insurance-funded buy-sell agreements, and the tax treatment differs significantly.

Structure: Each owner personally purchases life insurance policies on every other owner. When one owner dies, the surviving owners receive the death benefit from their personally owned policies and use it to purchase the deceased owner's shares directly.

How many policies are needed:

Tax advantage: The surviving owners get a stepped-up cost basis equal to the purchase price they paid for the deceased owner's shares. This matters significantly if they later sell the business.

Example: Three equal partners in a business valued at $6 million ($2M per partner). Partner A dies. Partners B and C each use their $1 million death benefit to buy half of Partner A's interest. Their cost basis in those acquired shares is now $1 million each. If they sell the business five years later for $10 million, they only pay capital gains tax on the appreciation from their stepped-up basis, not from their original basis.

Administrative complexity: More policies to manage, especially with 4+ partners. Each policy requires separate applications, underwriting, premium payments, and beneficiary designations. If a partner is added or leaves, policies must be restructured.

Premium payment structure: Each partner pays premiums on the policies they own. These are not business expenses and are paid with after-tax personal income.

When to use cross-purchase:

Structure: The business entity (corporation, LLC, or partnership) owns life insurance policies on all partners. When a partner dies, the business receives the death benefit and uses it to redeem the deceased owner's shares.

How many policies are needed:

Tax treatment consideration: In many entity-redemption structures, surviving owners don't receive the same direct purchase-basis step-up they would under a cross-purchase, which can increase future capital gains. The outcome varies by entity type and tax elections (such as IRC Section 754 elections for partnerships), so confirm the specific tax consequences with your CPA based on your entity structure.

Example: Same three-partner scenario. The business owns $2 million in coverage on Partner A. Partner A dies, business receives $2 million, redeems Partner A's shares. Partners B and C now own the entire business, but their cost basis is still their original investment (let's say $500k each). When they sell for $10 million, they pay capital gains tax on $9 million of gain ($10M sale price minus $1M combined original basis), rather than the reduced gain they'd have under cross-purchase.

Administrative simplicity: Fewer policies, simpler management. Business pays premiums from business cash flow; premiums are generally not tax-deductible. When partners join or leave, only one policy needs to be added or terminated.

Premium payment structure: Business pays premiums from business cash flow. Death benefits are received by the business income tax-free, though if the arrangement is treated as employer-owned life insurance under IRC 101(j), notice-and-consent and Form 8925 filing requirements apply.

Best practice on IRC 101(j): As a default, complete notice-and-consent for all entity-owned policies and file Form 8925 annually unless legal counsel confirms IRC 101(j) doesn't apply to your specific structure. The consequences of non-compliance (taxable death benefits) are severe enough that erring on the side of compliance is prudent. See detailed IRC 101(j) requirements in our complete guide to life insurance strategies for business owners.

When to use entity purchase:

Structure: The agreement gives the surviving owners the option to purchase the deceased owner's shares personally (like cross-purchase) or have the entity redeem them (like entity purchase). The decision is made after death based on the tax situation at that time.

Flexibility advantage: Allows the best tax treatment to be chosen based on circumstances that exist at the time of death, rather than locking into one structure years in advance.

Insurance structure: Typically structured as entity purchase for administrative simplicity. Wait-and-see agreements can allow flexibility in whether owners purchase personally or the entity redeems, but distributions and redemptions can have tax consequences depending on entity type, accumulated earnings, and individual tax situations. This must be drafted and modeled with tax counsel experienced in business succession.

Complexity: Requires sophisticated legal drafting to comply with IRS rules and avoid triggering transfer-for-value problems. Must be reviewed by a tax attorney experienced in business succession.

When to use wait-and-see:

Structure: A trust owns and administers all life insurance policies rather than individual partners owning policies on each other. When a partner dies, the trustee uses the death benefit to facilitate the purchase of shares by the surviving partners.

How it solves the policy explosion problem:

Tax treatment: When properly structured, the trustee purchases the deceased partner's shares and distributes them to the surviving partners, preserving the stepped-up basis benefit of a traditional cross-purchase.

Administrative advantage: One entity (the trust) collects premiums from all partners, pays all policies, handles beneficiary administration, and executes the buyout. Partners don't need to manage multiple policies on each other.

Legal complexity: Requires careful drafting to ensure the trust structure doesn't trigger transfer-for-value problems or accidentally create an entity purchase for tax purposes. The trust must be properly characterized and the purchase mechanics must flow through correctly.

When to use trusteed cross-purchase:

When NOT to use: 2-partner businesses where traditional cross-purchase only requires 2 policies (not enough complexity to justify the trust overhead).

The problem trusteed cross-purchase solves: In a traditional cross-purchase with 4+ partners, you end up with 12+ policies. Each partner is paying premiums on multiple policies, tracking multiple premium due dates, and managing multiple beneficiary designations. It becomes administratively unworkable.

How it works: A single trustee (often a trust company or designated partner) owns all the life insurance policies. When a partner dies, the trustee receives the death benefits and uses them to purchase the deceased partner's shares on behalf of the surviving partners. The surviving partners then own the shares individually (preserving the purchase-basis step-up concept).

Administrative advantage: One entity managing all policies, one set of premium payments to coordinate, one point of contact with carriers. Dramatically simpler than traditional cross-purchase for 4+ partners.

Tax treatment: When properly structured, this can still provide purchase-basis benefits similar to traditional cross-purchase, though the exact treatment depends on trust drafting and how the purchase mechanics are structured. This requires careful legal work.

Cost consideration: Using an institutional trustee adds annual trustee fees (typically $500-$2,000 per year depending on complexity). For partnerships with 5+ owners, this cost is often justified by the administrative simplification.

When to use trusteed cross-purchase:

Critical requirement: The trust document and buy-sell agreement must be integrated carefully to preserve tax treatment and avoid transfer-for-value issues. This is not a DIY structure. Work with attorneys experienced in trusteed buy-sells.

The life insurance death benefit should equal the business valuation formula specified in the buy-sell agreement. If there's a mismatch, you either have insufficient funds for the buyout (requiring debt or outside capital) or you're overpaying premiums for coverage you don't need.

1. Fixed Dollar Amount

How it works: The agreement states a specific dollar value (e.g., "$6 million for the entire business, $2 million per equal partner").

Advantage: Simple, no appraisal needed at death.

Disadvantage: Becomes outdated quickly. A business worth $6 million today might be worth $10 million in five years or $3 million after a market downturn. Requires annual updates to stay accurate.

When to use: Stable, mature businesses with predictable cash flows and no rapid growth expected.

Insurance implication: Coverage amount is fixed based on the stated value. Update policies whenever the agreement is amended with a new valuation.

2. Formula-Based Valuation (Multiple of Earnings)

How it works: Business value equals a multiple of EBITDA, revenue, or book value.

Common formulas:

Advantage: Automatically adjusts to business performance. No need to amend the agreement constantly.

Disadvantage: Can create disputes over which year's financials to use, adjustments for non-recurring items, or how to calculate EBITDA.

When to use: Growing businesses where value changes meaningfully year to year.

Insurance implication: Coverage amount should be set high enough to cover the formula at projected growth rates for the next 3-5 years. Review annually and increase coverage as business value grows.

Example: Business currently generates $2 million EBITDA. Agreement specifies valuation at 4× EBITDA. Current value: $8 million for three equal partners = $2.67 million per partner. If EBITDA is projected to grow 15% annually, in five years the business will be worth approximately $16 million ($4M EBITDA × 4). This illustrative projection suggests purchasing each partner at approximately $5.3 million in coverage to avoid being underinsured, though coverage should be reviewed annually and increased as actual valuation changes.

3. Independent Appraisal at Time of Death

How it works: Agreement requires an independent business valuation be conducted within 60-90 days of the triggering event. The appraised value determines the buyout price.

Advantage: Most accurate valuation based on current market conditions.

Disadvantage: Creates uncertainty about required funding, potential for disputes over appraisal methodology, delays the buyout until appraisal is complete.

When to use: Complex businesses with hard-to-value assets (intellectual property, customer contracts, real estate holdings).

Insurance implication: Coverage amount should be conservative (high enough to cover likely appraisal results). Consider a "floor and ceiling" approach where the agreement specifies minimum and maximum values to avoid extreme appraisals.

4. Regular Appraisal with Periodic Updates

How it works: Business is appraised every 2-3 years by an independent valuator. The most recent appraisal value is used for buyout purposes.

Advantage: Balance between accuracy and cost. Professional valuation without the delay of conducting one at death.

Disadvantage: Valuation can become stale between updates, particularly if significant changes occur (major client loss, new product launch, economic downturn).

When to use: Best practice for most established businesses with stable operations.

Insurance implication: Update coverage to match the appraisal each time it's conducted. This typically means increasing coverage every 2-3 years as the business grows.

Common sources of disputes:

Best practice: Include dispute resolution provisions in the agreement

Proper ownership and beneficiary structure is critical to avoid tax problems and ensure the buy-sell agreement works as intended.

Policy ownership: Each partner owns policies on the other partners.

Beneficiary designation: The policy owner is the beneficiary (not the insured's estate, not the business).

Example with 3 partners (A, B, C):

Premium payment: Each partner pays premiums on policies they own, typically from personal after-tax income.

At death: If Partner A dies, Partners B and C each receive death benefits from the policies they own on Partner A. They use this money to purchase Partner A's shares from the estate per the buy-sell agreement terms.

Critical mistake to avoid: Never name the insured's estate as beneficiary in a cross-purchase. The estate doesn't need the money; the surviving partners do (to buy the shares). If the estate receives the death benefit, it creates estate tax inclusion and the partners still need to find funds for the buyout.

Policy ownership: The business entity owns all policies on all partners.

Beneficiary designation: The business entity is the beneficiary.

Example with 3 partners:

Premium payment: Business pays premiums. Not tax-deductible, but simpler administration than cross-purchase.

At death: If Partner A dies, business receives the death benefit income tax-free (assuming IRC 101(j) compliance). Business uses the death benefit to redeem Partner A's shares from the estate.

IRC 101(j) compliance requirement: For employer-owned life insurance, the business must provide written notice to the insured and obtain written consent before the policy is issued. Without compliance, the death benefit is taxable income to the extent it exceeds premiums paid. File Form 8925 annually to report employer-owned policies. This is not optional. See detailed IRC 101(j) requirements in our complete guide to life insurance strategies for business owners.

The rule: If a life insurance policy is sold or transferred for valuable consideration, the death benefit becomes taxable income (minus premiums paid and consideration given).

Why this matters for buy-sell agreements: When restructuring ownership (converting from entity to cross-purchase, or vice versa), you may need to transfer policies. Triggering the transfer-for-value rule destroys the tax-free death benefit.

Safe harbor exceptions (transfers that don't trigger the rule):

Practical application: If you need to convert from entity purchase to cross-purchase:

When to get help: Any buy-sell restructuring involving policy transfers should be reviewed by a tax attorney before execution. The transfer-for-value rule has severe consequences and is easy to trigger unintentionally.

Most business owners use Guaranteed Universal Life (GUL) for buy-sell agreements rather than whole life or indexed universal life.

1. Lowest premium for guaranteed death benefit

GUL provides lifetime coverage to age 120 or 121 with level premiums. No cash value accumulation, which keeps costs low. For buy-sell purposes, you only care about the death benefit, not cash value growth.

2. Predictable costs for budgeting

Partners need to know what their annual premium commitment is for the duration of the agreement. GUL provides guaranteed level premiums that can't increase.

3. No performance risk

Whole life dividends and IUL credited interest vary. GUL has no moving parts related to market performance: pay the premium on time, get the guaranteed death benefit.

4. Minimal ongoing management

GUL policies require minimal ongoing management compared with cash-value-focused designs, but you still need an annual check to confirm premiums are current and guarantees remain intact. This matters when you have 6-12 policies in a multi-partner cross-purchase structure.

Whole life makes sense when:

Indexed universal life makes sense when:

Term life can work when:

Most common approach: GUL for permanent buy-sell agreements, term life with conversion rider for temporary situations.

Top carriers for buy-sell GUL coverage:

What to compare:

Underwriting considerations for business owners:

Working with an independent agency that has relationships with multiple carriers ensures you get the best underwriting outcome rather than being limited to one carrier's risk assessment.

The problem: Business is valued at $6 million when the buy-sell is signed. Five years later, it's worth $12 million. The life insurance coverage is still $6 million. A partner dies and the surviving partners only receive $6 million in insurance proceeds but owe the estate $12 million.

The fix: Annual policy reviews tied to business valuation updates. When the business grows, increase coverage. Most GUL policies allow coverage increases with evidence of insurability. Budget for periodic increases.

Best practice: Review coverage annually at the same time you file tax returns. If business value has increased more than 20%, increase coverage.

The problem: Original agreement covers three partners. A fourth partner is added but the buy-sell agreement isn't updated. Fourth partner dies and their estate sues, claiming they should have been included.

The fix: Amend the buy-sell agreement and update insurance coverage whenever ownership changes. This includes:

Best practice: Include a provision in the agreement requiring all new partners to join the buy-sell as a condition of ownership.

The problem: Buy-sell agreement covers death but not disability. Partner becomes permanently disabled, can't work, but remains on the cap table. Surviving partners are running the business while disabled partner collects distributions without contributing.

The fix: Add disability buyout provisions to the agreement and fund with disability buyout insurance. Typical structure:

Disability buyout insurance: Separate from disability income insurance. Pays a lump sum to fund the buyout after the waiting period. More expensive than life insurance (typically 3-5× the premium for comparable coverage) because disability is more likely than death.

Best practice: At minimum, include disability buyout provisions in the agreement even if you don't fund with insurance initially. This prevents disputes about whether the disabled partner should be bought out.

The problem: Agreement specifies book value but business has significant intangible assets (goodwill, customer relationships, brand value) not reflected on the balance sheet. Deceased partner's estate sues claiming the buyout price is too low.

The fix: Use fair market value or EBITDA-based formulas for most operating businesses. Book value only works for asset-heavy businesses (real estate, equipment leasing) where book value approximates market value.

Best practice: Have the business appraised when the buy-sell is first signed. Use that appraisal to set the initial coverage amount and validate that the valuation formula produces reasonable results.

The problem: Deceased partner's estate plan directs that business interests pass to a trust for the benefit of their children. Buy-sell agreement requires the estate to sell the shares to surviving partners. Trust and estate compete for control of the shares, creating litigation.

The fix: Coordinate buy-sell agreement with each partner's estate plan. The estate plan should acknowledge the buy-sell agreement and direct the estate to comply with its terms.

Best practice: Each partner should provide their estate planning attorney with a copy of the buy-sell agreement. The will or trust should include language like: "I acknowledge that my business interests in [Company Name] are subject to a buy-sell agreement dated [date], and I direct my executor/trustee to comply with its terms."

The problem: Agreement is signed, policies are purchased, then partners stop paying premiums after two years. Policies lapse. Partner dies, no death benefit, surviving partners scramble for capital.

The fix:

Best practice: Annual meeting to review all policies, confirm premiums are current, update coverage as needed. Make this part of the annual shareholder/partner meeting agenda.

Use this checklist to ensure your buy-sell agreement is properly structured and funded:

Legal documentation:☐ Buy-sell agreement drafted by attorney experienced in business succession

☐ Agreement specifies triggering events (death, disability, retirement, divorce, bankruptcy, voluntary departure)

☐ Valuation method clearly defined with dispute resolution provisions

☐ Funding mechanism specified (insurance required, timeline for buyout)

☐ All partners have signed the agreement

☐ Agreement is attached as exhibit to operating agreement or corporate bylaws

Life insurance funding:☐ Decide between cross-purchase, entity purchase, or wait-and-see structure

☐ Calculate coverage amount based on current valuation

☐ Obtain quotes from multiple carriers

☐ Submit applications with proper ownership and beneficiary designations

☐ Policies issued and premiums current

☐ Copy of each policy attached to buy-sell agreement as exhibit

Tax and compliance:☐ If entity purchase: IRC 101(j) notice and consent completed before policy issue

☐ If entity purchase: Form 8925 filed annually

☐ Transfer-for-value rule reviewed if converting between structures

☐ Estate planning documents for each partner reference the buy-sell agreement

Ongoing administration:☐ Annual review scheduled (same time as tax filing or shareholder meeting)

☐ Insurance administrator appointed to track premiums and coverage

☐ Valuation update schedule established (every 2-3 years minimum)

☐ Process for adding new partners documented

☐ Process for increasing coverage as business grows documented

A properly structured and funded buy-sell agreement protects your business from forced liquidation, prevents disputes among partners and their heirs, and ensures smooth ownership transitions without disrupting operations.

Questions to ask yourself:

If you answered no to any of these questions, or haven't reviewed your buy-sell agreement in the last two years, it's time for an update.

Ready to structure or update your buy-sell agreement?

Living Equity Group works with business owners to design buy-sell funding strategies using life insurance from top carriers including AIG, Banner, Lincoln Financial, Pacific Life, and Nationwide. We coordinate with your attorney and CPA to ensure the insurance structure matches your legal agreement and tax objectives.

This allows us to identify coverage gaps, confirm proper policy ownership and beneficiary designations, and recommend coverage adjustments to match current business value.

Schedule a buy-sell agreement review →

Related Resources:

About Living Equity Group

Living Equity Group specializes in business succession planning and advanced life insurance strategies for multi-owner businesses. We handle all underwriting coordination, carrier communication, and policy administration while working seamlessly with your legal and tax advisors to ensure your buy-sell agreement works exactly as intended.

Questions? Contact our team at cases@livingequitygroupllc.com.