When most people think of retirement planning, they think of 401(k)s and IRAs. But these accounts come with contribution limits, income phaseouts, and taxable distributions. That’s why high-income earners and high-net-worth individuals often need additional tools that offer tax-advantaged growth and accessible income later in life.

One of the most underutilized, but powerful, retirement vehicles is Indexed Universal Life (IUL). It’s not just insurance. It’s a flexible, tax-efficient savings strategy disguised as a life insurance policy.

An IUL is a permanent life insurance policy that allows the insured to contribute premium payments beyond what’s needed for insurance costs. These excess premiums go into a cash value account that grows based on the performance of a stock market index (commonly the S&P 500).

As the cash value grows:

At retirement, clients can draw on the policy’s cash value to supplement other income sources often generating 7–9% average returns, with no taxes owed on distributions.

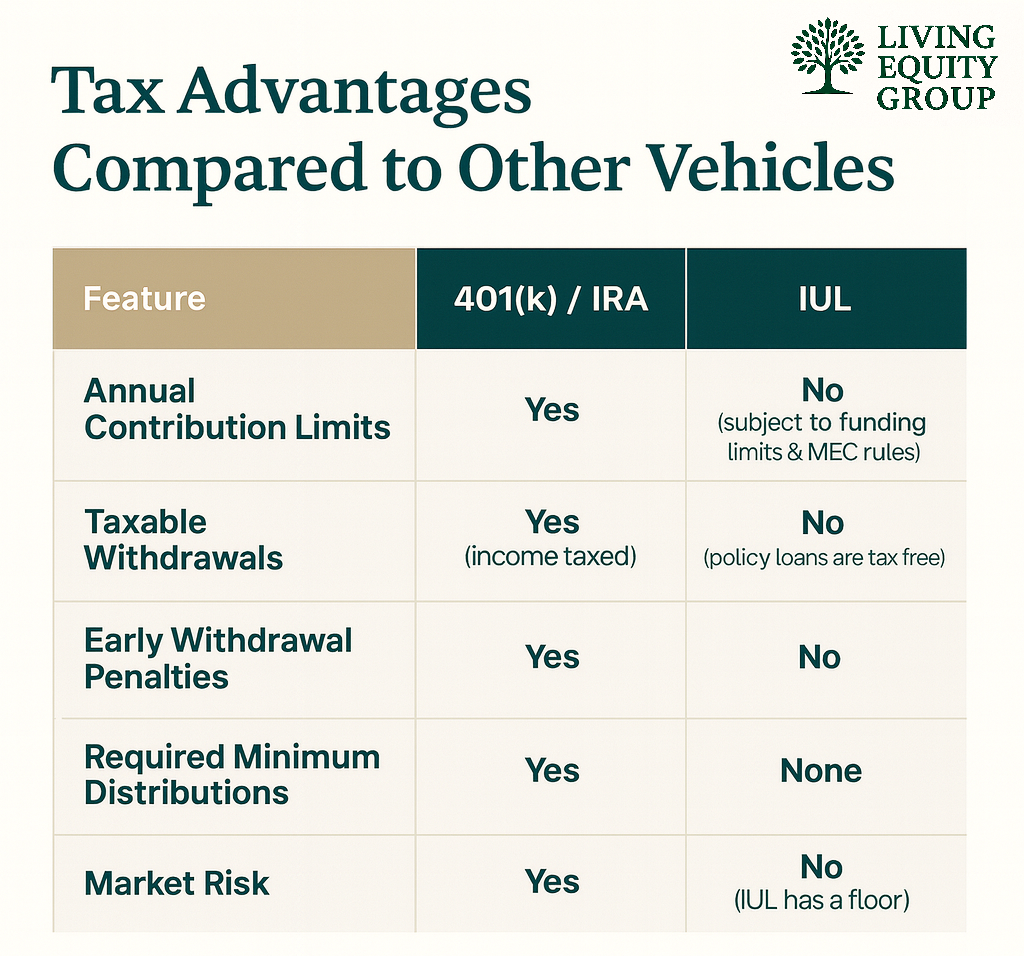

Let’s compare IUL to other common retirement options:

For clients in high tax brackets, the ability to accumulate and access retirement income tax-free makes IUL a uniquely powerful tool.

IUL policies are linked to market index performance, but unlike traditional investments, they include built-in floors and caps:

This means:

✔️ Clients participate in up markets

❌ Without losing money in down years

Over time, this balance tends to deliver consistent long-term growth, without the stress of market timing.

Not all IULs are created equal. To work effectively as a retirement planning tool, the policy must be:

That’s why working with a back office like Living Equity Group can help brokers optimize for retirement outcomes, not just coverage.

When designed correctly, IUL policies give clients the best of all worlds:

For brokers, it’s a compelling way to reframe life insurance as an investment with an insurance wrapper, especially for clients who are maxing out other retirement vehicles or looking to avoid future tax exposure.

💡 Want help designing an IUL retirement plan for your next client? Submit a case to LEG and we’ll help build it from start to finish.