Choosing the right type of life insurance is one of the biggest financial decisions you’ll make. The two most common options — term life insurance, whole life insurance, and index universal life — serve different purposes and come with very different price tags.

If you’ve ever wondered “Which is better for me?” you’re not alone. This guide explains how each works, the pros and cons, and how to decide which one fits your needs.

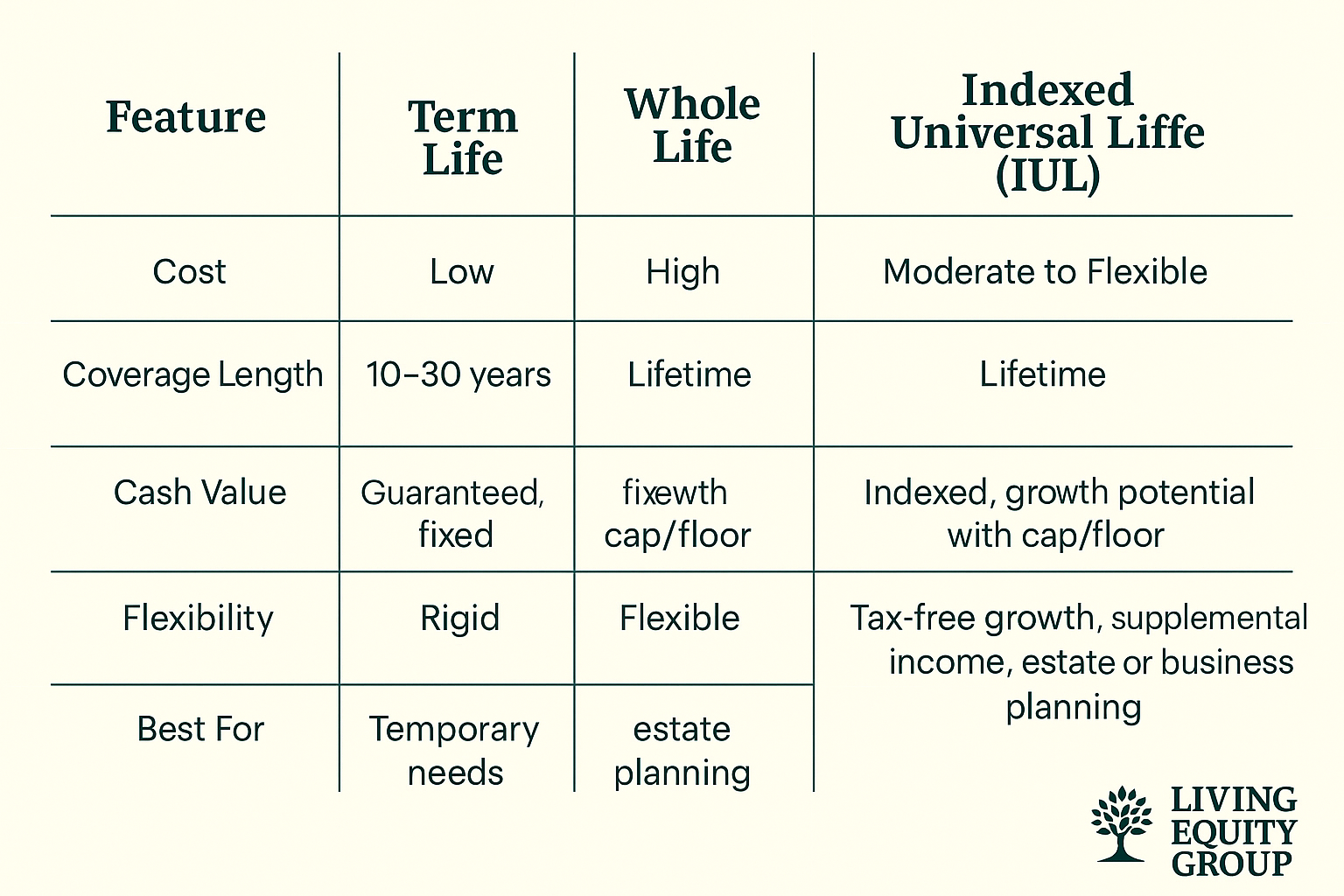

Term life insurance provides coverage for a set period, usually 10, 20, or 30 years. If the insured dies during the term, beneficiaries receive the policy’s death benefit.

💡 Example: A 30-year-old could buy a 20-year, $500,000 term policy for as little as $25/month.

Whole life insurance is a permanent policy that lasts for the insured’s entire life, as long as premiums are paid.

💡 Example: That same 30-year-old may pay $400+/month for a $500,000 whole life policy, but part of the premium goes toward building cash value.

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that offers flexible premiums, lifetime coverage, and the ability to build cash value based on the performance of a stock market index, such as the S&P 500. While the cash value grows in relation to market index performance, the policy is protected from loss through built-in floors—so the value won't decrease even if the market does.

Unlike whole life, IUL policies offer adjustable death benefits and custom allocation strategies, making them highly attractive for high-net-worth individuals looking to:

Because of their growth potential, flexibility, and downside protection, IULs are often used in advanced planning strategies, especially for clients who want more than just a death benefit.

💡 Example: That same 30-year-old might pay $200–$300/month for a $500,000 IUL policy, with potential for future cash value accumulation that can be accessed tax-free in retirement.

While term and whole life insurance are often seen as the two primary options, many high-net-worth clients benefit from a third type: Indexed Universal Life (IUL). IUL blends features from both term and permanent insurance, offering lifelong coverage with flexible premiums and the potential to build tax-deferred cash value based on index performance (like the S&P 500). For clients seeking income planning, estate protection, and market participation without downside risk, IUL can be a powerful tool.

✅ Pros

❌ Cons

✅ Pros

❌ Cons

✅ Pros

❌ Cons

There’s no one-size-fits-all answer. Here’s how to decide:

The difference between term and whole life insurance comes down to cost vs. permanence. Term life offers simple, affordable coverage for a set time. Whole life provides lifelong protection and a cash value component, but at a much higher cost. While term and whole life serve many clients well, brokers working with high-net-worth individuals often find Indexed Universal Life (IUL) offers the most strategic flexibility. At Living Equity Group, we specialize in designing custom IUL solutions tailored to income, estate, and business planning goals.